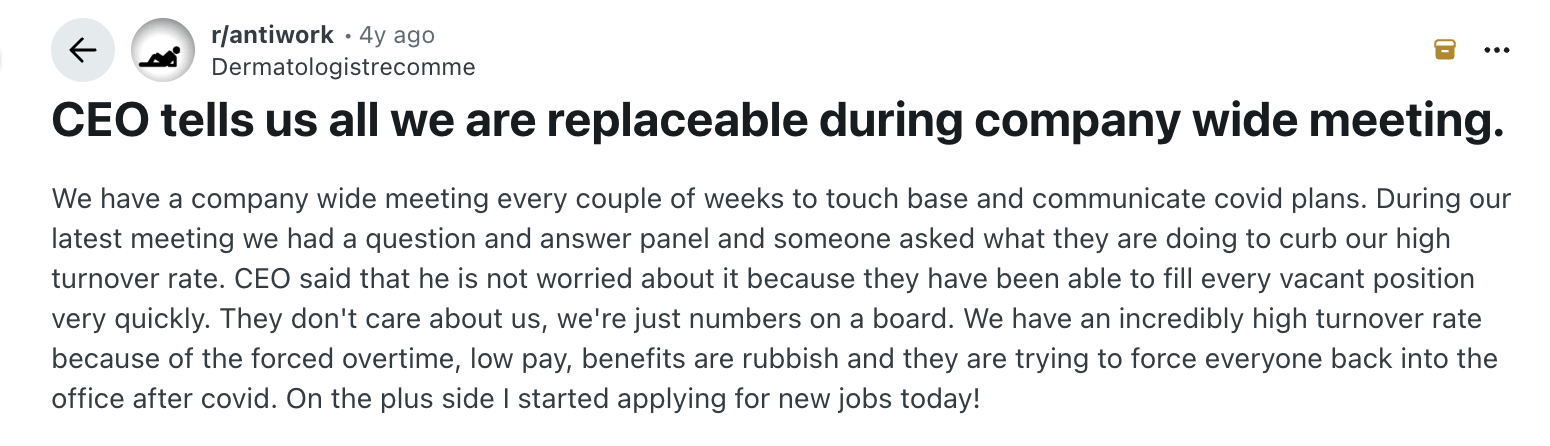

A CEO who told employees they were “all replaceable” in a company-wide meeting saw his remarks resurface online after the firm filed for Chapter 11 bankruptcy just two months later, according to a viral Reddit post that has fuelled debate over leadership and corporate accountability.

The post, shared on the r/work forum, described how the executive attempted to “motivate” staff by warning them about performance and replaceability. Within 60 days, the company sought bankruptcy protection. Jobs were cut, severance terms became uncertain and employees faced disruptions to health benefits, the post claimed.

While the specific company was not publicly identified, the episode comes against a broader backdrop of rising corporate insolvencies in the United States.

According to federal court data, overall US bankruptcy filings increased by nearly 18% year on year in 2025. Corporate Chapter 11 filings also rose sharply, with small and mid-sized companies particularly affected. Total filings exceeded 450,000 cases in the past year, with business bankruptcies accounting for a growing share.

Chapter 11 allows companies to restructure debt while continuing operations. In practice, restructuring frequently involves layoffs, asset sales and contract renegotiations, leaving employees facing immediate uncertainty.

The viral story has resonated widely because it mirrors a pattern seen in recent insolvency cases. Executives often intensify messaging around productivity, cost control and performance in the weeks or months preceding financial distress becoming public.

Labour market surveys show that employee morale remains a critical factor in retention. Recent data indicates that 79% of workers who leave their jobs cite lack of appreciation as a primary reason. Management research, including Gallup workplace studies, consistently finds that fear-based leadership reduces engagement and productivity.

Economic analysts attribute the rise in corporate bankruptcies to several factors: higher interest rates, increased debt servicing costs, slower revenue growth, reduced venture capital funding and tighter lending standards. Companies that expanded aggressively during periods of low borrowing costs now face refinancing pressures at higher rates.

Public filings in some recent bankruptcy cases have shown executive bonuses paid months before insolvency declarations, raising questions about governance and disclosure practices. The Securities and Exchange Commission requires public companies to disclose material financial risks, but private firms face fewer reporting obligations, leaving employees with limited visibility into emerging distress.

When a company files for bankruptcy, employees confront immediate practical concerns: wage continuity, healthcare coverage, severance terms and retirement contributions. Under US law, unpaid wages may qualify as priority claims, but full recovery is not guaranteed. State labour departments often report spikes in unemployment claims following major Chapter 11 filings.

Corporate governance experts note that bankruptcy rarely occurs overnight. Financial warning signs — declining revenues, rising debt, hiring freezes and delayed payments — typically accumulate over months. Employees, however, are often informed only at the point of filing.

The Reddit episode has intensified discussion around executive messaging during periods of financial strain. Analysts say leadership tone can influence morale, retention and even operational resilience in distressed companies.

As bankruptcy filings continue to rise in 2026, the broader debate is shifting towards transparency, governance discipline and worker protection. The viral story serves as a reminder that corporate solvency hinges on strategic and financial decisions taken at the top — decisions employees rarely control, but frequently bear the consequences of.